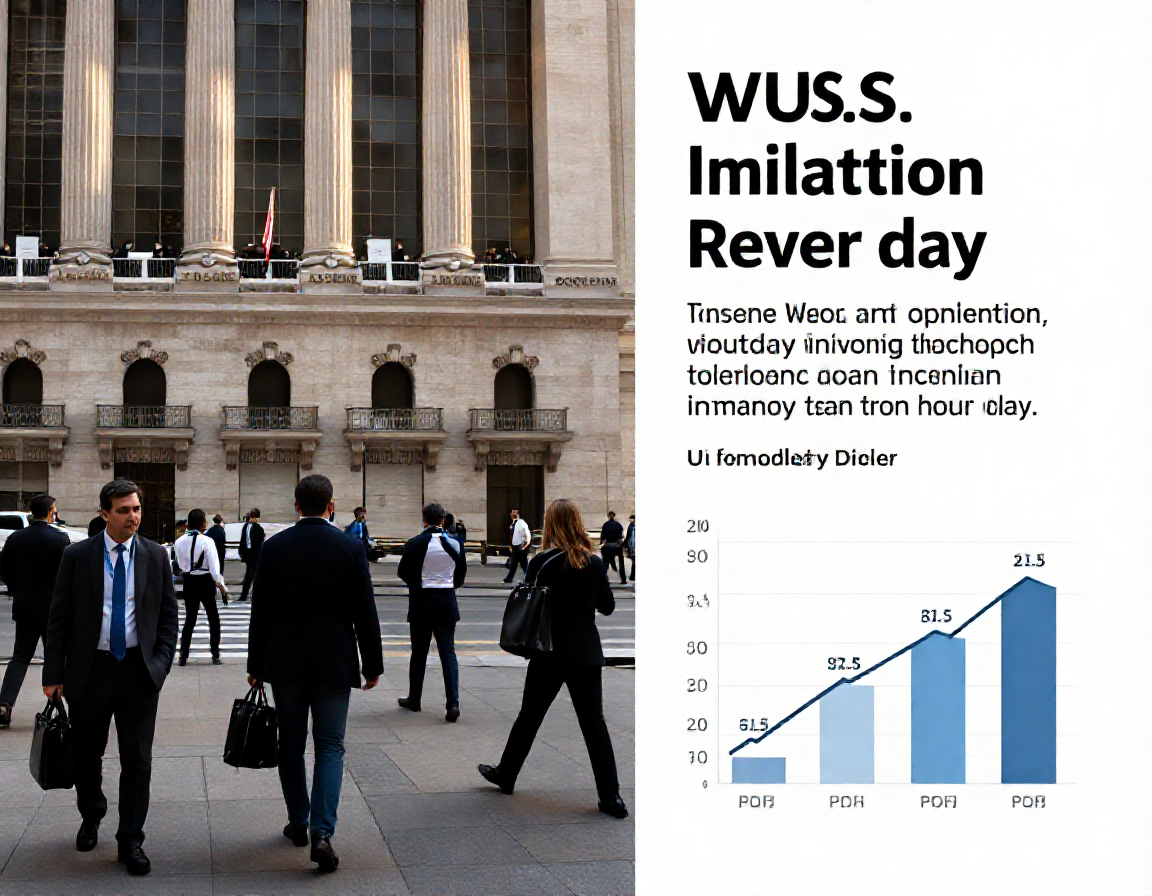

1. Why Inflation Release Days Matter in 2026

Inflation release days are no longer routine calendar events; they are policy-transmission events. In 2026, U.S. equities react quickly because one data print can alter the expected path of policy rates, real yields, and discount rates used in valuation models. When that policy path shifts, the market does not wait for full confirmation. Index futures, options positioning, and systematic flows can move first, while discretionary investors recalibrate exposure afterward.

From a structural perspective, the speed of repricing is not just about “good” or “bad” inflation. It is about how far the print lands from consensus, how broad the surprise is across categories, and whether the surprise changes the probability of future Federal Reserve actions. Market participants appear to be pricing in this chain immediately: inflation surprise to rates repricing, rates repricing to equity multiple adjustment, and multiple adjustment to sector rotation.

This matters because many investors still evaluate inflation prints as single-point headlines. Professional positioning requires a process view: what changed in policy expectations, what changed in financial conditions, and what changed in earnings-risk tolerance. Without that sequence, investors may overreact to the first move or miss the second-wave repricing that often occurs once rates and volatility markets settle.

2. The Transmission Channel: From Data Surprise to Equity Repricing

The first link in the chain is the data surprise relative to market expectations. If core inflation prints above consensus, front-end yields often move higher as implied policy easing is delayed. If the miss is broad across services and wage-sensitive components, the move can extend beyond the first minutes. If the surprise is concentrated in volatile categories, the first move may fade.

The second link is real yields. Equity valuation is especially sensitive to real-rate direction because real yields affect the present value of future cash flows. When real yields rise quickly, long-duration equity segments can face multiple compression even if earnings forecasts are unchanged. Conversely, when inflation cools and real yields stabilize, valuation pressure can ease and market breadth can improve.

The third link is volatility and positioning. If implied volatility rises while yields move against prior consensus, de-risking flows can amplify equity downside. If volatility remains contained and rates retrace, the initial equity move can reverse. Liquidity conditions suggest that the first 15–30 minutes capture directional shock, while the next one to two hours often determine whether the move is durable.

3. Reading Inflation Prints Beyond the Headline

Headline CPI alone is not enough. Investors should separate trend information from noise by focusing on composition and breadth. A practical framework is to evaluate three layers: persistence, breadth, and policy relevance.

Persistence asks whether the drivers are likely to repeat next month. Breadth asks whether pressure is concentrated or widespread. Policy relevance asks whether the surprise changes the reaction function implied by Federal Reserve communication. For example, a small upside surprise driven by one-off components may not materially alter policy expectations. But a broad upside in core services can shift the expected timing of easing and therefore move both rates and equities.

Another key point is base effects and prior revisions. A seemingly benign headline can still tighten policy expectations if prior months are revised upward. Likewise, a soft print can have limited impact if labor-market and wage data remain firm. From a practical investment perspective, inflation interpretation should be integrated with payroll trends, wage growth, and survey-based inflation expectations rather than treated in isolation.

4. Real-Time Market Dashboard for Release Days

On release days, investors can use a real-time dashboard to avoid emotional decisions. Four indicators are especially useful: two-year Treasury yield, five-year real yield, S&P futures breadth, and the VIX term structure.

If two-year yields rise, five-year real yields rise, breadth narrows, and near-term volatility steepens, the market is signaling tighter financial conditions. In that setup, equity downside can extend beyond the opening impulse. If yields rise but volatility remains stable and breadth recovers quickly, the market may be pricing the surprise as manageable rather than regime-changing.

Execution quality improves when investors predefine thresholds. For instance, a basis-point move in front-end yields beyond a preset range can trigger a partial risk reduction rather than a full de-risking. A volatility spike without cross-asset confirmation can call for patience instead of immediate position changes. The goal is consistency, not speed for its own sake.

Institutional desks typically separate tactical reaction from strategic allocation. Tactical books respond to intraday signal quality; strategic books wait for confirmation in policy communication, rates persistence, and credit behavior. Adopting that separation helps individual investors avoid overtrading around noisy first moves.

5. Scenario-Based Portfolio Responses

A scenario framework is essential in 2026 because inflation outcomes can produce very different policy and market paths. In a base case, inflation gradually cools with mixed monthly prints, allowing policy expectations to normalize without major dislocation. In that regime, selective risk-taking is reasonable, especially in sectors with earnings durability and balance-sheet strength.

In a hawkish case, repeated upside surprises in core inflation can delay expected easing, keep real yields elevated, and pressure valuation-sensitive equities. Portfolio response should emphasize risk control, cash-flow quality, and disciplined position sizing. In a dovish case, downside inflation surprises combined with stable growth can support lower real yields and broader equity participation, but investors should still avoid concentration risk.

What matters most is not calling every print correctly, but preparing decision rules before the release. Investors can define allocation bands for each scenario, set rebalance triggers, and cap drawdown tolerance. This turns inflation days from reactive events into managed process checkpoints.

6. Strategic Conclusion: Process Over Prediction

The strategic takeaway is simple: inflation print days are high-frequency tests of macro discipline. Markets reprice within minutes because policy expectations, discount rates, and risk appetite are jointly repriced. Investors who rely on headlines alone are vulnerable to whipsaw; investors with a repeatable framework can respond with higher consistency.

A robust playbook includes pre-release scenario mapping, intraday cross-asset verification, and post-release reassessment of policy path assumptions. Position changes should be linked to evidence quality: broad inflation surprise, rates confirmation, and volatility regime shift. If only one signal changes, smaller adjustments are usually superior to aggressive reallocation.

Over time, process quality compounds.